Search Our Blog

Tax policy rarely grabs headlines in the taxi sector, but recent changes to the way VAT is applied to ride‑hailing fares have created significant debate across the industry. The UK government introduced new rules designed to ensure the full value of minicab fares is subject to VAT when processed through platforms such as Uber. The measure was expected to raise hundreds of millions of pounds in tax revenue each year. However, the situation quickly became more complicated. Uber’s Contract Changes In response to the new tax rules, Uber revised its contracts with drivers across much of the UK. Under the revised structure, Uber positions itself as an agent connecting passengers with drivers rather than the supplier of the transport service itself. This change means drivers technically provide the service and are responsible for charging VAT if required. Why the Tax May Not Apply to Many Fares Most private‑hire drivers earn less than the UK VAT registration threshold, which currently sits at £90,000 in annual revenue. If a driver earns below that level, they do not have to register for VAT. That means the 20% tax will not be added to their fares. As a result, many rides booked through Uber outside London may continue to avoid the VAT increase that policymakers expected to see. Differences in London The situation is different in London. Transport for London requires ride‑hailing platforms to operate under a model where the platform is considered the transport provider. Because of that rule, VAT still applies to the full fare in the capital. This creates an unusual situation where the same ride‑hailing company operates under different tax structures depending on where the journey takes place. Impact on the Taxi Industry For traditional taxi and private‑hire operators, the issue is not just about tax. The way ride‑hailing companies structure their contracts affects pricing, competition and driver earnings. Changes to VAT rules can influence fare levels and therefore demand. Some industry figures argue that the rules should be clearer so that all operators compete under similar tax conditions. What Drivers Should Watch Drivers need to pay close attention to how their contracts are structured and how tax obligations apply to them. If earnings rise above the VAT threshold, drivers may be required to register for VAT and charge it on fares. That could affect both pricing and income. Understanding these rules is becoming an important part of running a private‑hire business. Looking Forward The taxi sector has always adapted to regulatory change. The current VAT debate is another example of how legal and tax frameworks can reshape the economics of ride‑hailing. For drivers, operators and platforms, staying informed about these changes will be essential as the industry continues to evolve.

London is preparing for a major shift in urban transport as several companies plan to introduce driverless taxis in the city over the next year. Ride‑hailing platforms including Uber and Lyft are working with Chinese technology firm Baidu to launch autonomous taxi trials in 2026. The vehicles will use Baidu’s Apollo Go self‑driving system, which has already been deployed in cities across China. The trials are part of the UK government’s effort to accelerate autonomous vehicle development. Britain wants to position itself as a leading market for this technology, and London’s dense traffic environment makes it an ideal testing ground. Why London Matters London is one of the world’s most complex driving environments. Narrow roads, heavy pedestrian traffic, cyclists and buses all create challenges that autonomous systems must learn to handle. Because of this complexity, companies often train their systems in stages. Vehicles initially operate with safety drivers while they collect mapping data and learn how to respond to local road behaviour. Alphabet’s autonomous vehicle division Waymo is already carrying out this process. Its cars have been spotted driving around London with human operators behind the wheel while the technology is refined. How Robotaxi Fleets Work Autonomous taxis operate differently from traditional taxi services. Instead of individual drivers owning or leasing vehicles, robotaxis are typically run as large fleets managed by technology companies or mobility platforms. The vehicles are designed to operate for long hours with minimal downtime. This changes the business model. Revenue depends on vehicle utilisation rather than driver shifts. Fleet operators focus on charging infrastructure, maintenance schedules and software updates rather than driver recruitment. For the taxi and private‑hire sector, that means the industry may gradually move toward a mix of human‑driven and autonomous services. What It Means for Drivers Robotaxis are unlikely to replace human drivers in the short term. Early deployments will involve small fleets operating in limited areas while regulators monitor safety. Drivers still provide services that technology struggles to replicate, such as assisting passengers with accessibility needs, handling unusual journeys or navigating unpredictable traffic conditions. However, automation could change parts of the market. Short, routine journeys may eventually be served by autonomous vehicles while drivers focus on premium, specialist or high‑service trips. Regulation and Safety The legal framework for self‑driving vehicles is being established through the Automated Vehicles Act, which sets rules on liability and operational responsibility. Under the new system, the company operating the autonomous vehicle — not the passenger — will be responsible if something goes wrong. This approach is intended to provide clarity for insurers, regulators and the public. The Road Ahead Robotaxi trials in London represent the first real test of autonomous ride‑hailing in the UK. The technology has already logged millions of miles in the United States, but London presents a completely different challenge. If the trials succeed, they could mark the beginning of a gradual transformation in how taxi services operate across the country.

The UK government is moving toward national minimum standards for taxi and private‑hire licensing, alongside the possibility of larger regional licensing areas. The aim is to reduce inconsistencies between councils and improve passenger safety across England. At present, licensing rules vary widely between local authorities. This affects driver vetting, vehicle requirements and enforcement capacity. It also allows drivers licensed in one area to work predominantly in another, which has long been a point of tension within the industry. National standards would introduce consistent background checks, safety requirements and accessibility rules. For passengers, that means greater confidence that any licensed vehicle meets the same baseline. For drivers, it could mean clearer expectations but also more rigorous compliance. Operators may face transitional costs as systems and documentation are aligned with new rules. However, greater consistency can reduce long‑term administrative complexity, particularly for businesses operating across multiple regions. Larger licensing areas are also being considered. This could improve enforcement by aligning licensing with wider transport authorities rather than individual councils. It may also make it easier to share data and carry out joint compliance operations. For fleet owners and finance providers, regulatory clarity is positive. Consistent standards reduce uncertainty when assessing risk across different regions. Vehicles operating under a uniform framework are easier to value and finance than those subject to highly localised rules. Drivers will need to monitor consultation outcomes closely. Changes to medical checks, training requirements or safeguarding standards could affect licence renewals. Planning ahead and keeping documentation current will be essential to avoid interruptions to work. The reforms are still in development, and industry input will shape the final framework. However, the direction is clear: stronger safety oversight and more consistent licensing across the country. For the UK taxi and private‑hire sector, this is a structural change rather than a short‑term adjustment. Businesses that invest early in compliance systems, driver training and clear governance will find the transition smoother and be better positioned for future regulatory developments, including the integration of autonomous vehicles.

The launch of Uber’s new autonomous services division shows that the focus in the robotaxi sector is shifting. The technology is no longer the only story. The real question now is how these vehicles will be funded, maintained and integrated into working fleets. For the UK taxi and private‑hire market, this is highly relevant. London is expected to host early robotaxi trials in 2026, and while the fleets will be small, the support systems behind them will be significant. Charging networks, insurance models, real‑time monitoring and vehicle lifecycle management will all need to be in place before large‑scale deployment. This creates a new layer in the market. Traditional operators focused on drivers and dispatch. Autonomous fleets shift attention to asset utilisation, uptime and maintenance planning. A vehicle that can run longer hours without driver limits changes revenue patterns but also increases pressure on reliability and servicing schedules. Finance structures will also evolve. Robotaxis are capital‑intensive assets with high upfront costs but potentially longer operating hours. That means lenders and brokers will need to model different cashflow patterns compared with conventional private‑hire vehicles. Residual values, software upgrades and battery health become key variables in risk assessment. There is also a regulatory dimension. UK authorities are working on safety frameworks for autonomous vehicles. Operators involved in early pilots will need robust compliance systems, detailed reporting and clear accountability for incidents. The bar for governance will be high. Human drivers are not disappearing in the short term. Early deployments will run alongside conventional taxis and private hire vehicles. However, roles may shift toward fleet supervision, customer support and specialist services where human interaction is essential. For operators and asset partners, the practical step is to start planning for mixed fleets. Understanding utilisation metrics, maintenance intervals and financing structures for high‑value vehicles will be essential. The businesses that adapt early to asset‑led operating models will be better positioned as autonomy scales. Robotaxis are often presented as a technology story. In reality, they are an infrastructure and finance story. The companies that understand how to fund, manage and regulate these assets will shape the next phase of the UK taxi market.

Lancaster City Council’s decision to grant Uber a local private‑hire operator licence marks a notable change in how ride‑hailing services are regulated at a local level. Previously, many Uber drivers working in the district were licensed by other authorities, which meant Lancaster had limited power to investigate complaints or enforce standards. By issuing a local operator licence, the council has brought those activities within its own regulatory framework. That gives licensing officers clearer authority to inspect vehicles, review driver conduct and respond to passenger concerns. For local residents, it means the same rules apply to Uber as to any other private‑hire operator based in the area. The move also reflects a wider national debate about out‑of‑area licensing. Councils have long argued that when drivers are licensed elsewhere but work locally, enforcement becomes more difficult. Local licensing is seen as a way to improve accountability and ensure consistent standards across all operators. For Uber, obtaining a local licence can strengthen relationships with councils and demonstrate willingness to comply with local requirements. It may also reduce friction with traditional taxi and private‑hire firms that have argued for a level playing field. However, it comes with additional administrative responsibilities and ongoing scrutiny. Local operators are watching closely. Where a major platform is regulated under the same framework, there is greater confidence that enforcement will be applied consistently. That can help stabilise local markets and reduce tensions between different parts of the trade. There are financial implications as well. Local licensing can affect vehicle numbers, driver onboarding times and compliance costs. For fleet investors and brokers, understanding which authority licenses a vehicle or operator is important when assessing utilisation risk. A vehicle tied to a licence that restricts where it can work may generate different revenue compared with one operating across multiple districts. Passengers may notice little day‑to‑day difference, but the regulatory shift matters behind the scenes. Local oversight makes it easier to handle complaints, monitor safety and maintain service standards. In the long run, that can support public confidence in app‑based private‑hire services. Lancaster’s decision is unlikely to be the last of its kind. As councils seek more control over services operating in their areas, more platforms may apply for local licences rather than relying on drivers licensed elsewhere. That trend would move the sector toward clearer lines of accountability and more consistent regulation across the country.

Safety enforcement has moved back into the spotlight after Transport for London confirmed that nearly 500 private‑hire driver licences were revoked over the past year. The reasons included drink‑driving, drug disqualifications, serious misconduct and other offences that raised concerns about whether drivers were “fit and proper” to carry passengers. For passengers, the message is clear: the regulator is willing to act quickly where risk is identified. TfL does not always wait for a court conviction before removing a licence if there is strong evidence that public safety could be affected. That approach is designed to protect vulnerable users and maintain confidence in licensed services. For drivers, the implications are more complex. Many work long hours in a competitive market where earnings can be unpredictable. Compliance requirements, medical checks and background screening add to the administrative load. However, the data shows that failing to meet those standards can end a driver’s ability to work in the capital almost immediately. Operators and platforms also feel the impact. Licence revocations can reduce available drivers, particularly during peak periods, and increase recruitment and onboarding costs. They also carry reputational risk. Passengers expect licensed services to be safe, and any high‑profile enforcement action can affect brand perception across an entire platform, not just the individuals involved. Outside London, enforcement is often less centralised. Many areas rely on smaller licensing teams with fewer resources, which can make consistent monitoring more difficult. That difference is one reason why out‑of‑area licensing remains controversial. A driver licensed in one district may spend most of their time working in another where enforcement powers are limited. For fleet owners and finance partners, safety compliance should be treated as a core business risk rather than a background process. Vehicles that cannot legally operate due to driver issues generate no revenue but still incur costs. Strong onboarding checks, regular training and clear reporting procedures reduce the likelihood of disruption. There is also a forward‑looking angle. As autonomous vehicle pilots move closer to commercial reality, regulators will expect even higher standards of data reporting, incident management and operational transparency. Companies that already have robust compliance systems will find that transition easier. The headline figure of hundreds of revoked licences is not just a statistic. It is a signal that safety oversight is active and that regulatory expectations are rising. For drivers, operators and asset partners, the practical response is straightforward: keep documentation current, invest in compliance processes and treat safety as central to commercial performance rather than an administrative afterthought.

Autonomous taxi services could arrive on UK roads later this year as regulatory frameworks evolve. Plans are advancing to update legislation in the second half of 2026 to allow fully driverless taxis to operate commercially. Several major technology and ride‑hailing companies are preparing for this shift, which has far‑reaching implications for the taxi and private‑hire industry. Regulatory Changes and Pilot Services The UK government has signalled that it will update regulations to permit fully driverless vehicles to operate as passenger‑carrying taxis. Until now, trials have operated with safety drivers in place, and passenger trials are expected under controlled arrangements. Waymo, an autonomous ride‑hailing specialist, has said it hopes to launch a robotaxi service in London as early as September 2026, using vehicles compliant with new rules once they are enacted. Regulatory approval will be required before these services can operate without a human driver present. Britain’s Automated Vehicles Act provides the legal basis for this shift, but regulators must still define specific safety standards and certification processes. These will cover everything from object detection and emergency response to cybersecurity protections against hacking threats. Governments emphasise that autonomous taxis must be at least as safe as careful human drivers to be allowed on public roads. Industry Players and Competition Waymo isn’t alone in its ambitions. Ride‑hailing firms like Uber and Lyft are planning autonomous taxi introductions once the regulatory framework is in place. Partnerships with technology firms, including Chinese partners, are part of these plans. Strong competition among operators could drive rapid technology adoption, but also increase pressure on traditional drivers and operators to adapt. What It Means for Drivers Driverless taxis raise questions about the future role of human drivers in urban transport. In the near term, these services will operate alongside conventional taxis and private‑hire vehicles. Traditional drivers may find new roles in on‑boarding, oversight or customer support for autonomous fleets. However, there’s also concern that automation could displace demand for conventional driver work over time. Opportunities for Operators and Brokers Operators and brokers have a chance to engage early with the regulatory process and understand how autonomous services could complement existing networks. For example, robotaxis could handle high‑density routes while human drivers focus on more complex routes or passenger groups that prefer personalised service. Fleet financing partners should build scenarios that include autonomous assets, factoring in potential shifts in utilisation, revenue and residual values. Challenges Ahead Public trust is a major hurdle. Passengers need assurance that driverless taxis are safe, reliable and secure. Regulators, operators and technology companies must demonstrate safety performance through robust testing and transparent reporting. Additionally, infrastructure such as digital mapping, communication systems and roadside support will need investment. Looking Ahead The introduction of driverless taxis in the UK represents a major shift for the sector. If regulations fall into place as expected in the second half of 2026, London could be a launchpad for commercial robotaxi services. Careful planning, collaboration between industry and regulators, and clear communication with drivers and passengers will be essential to make this transition work.

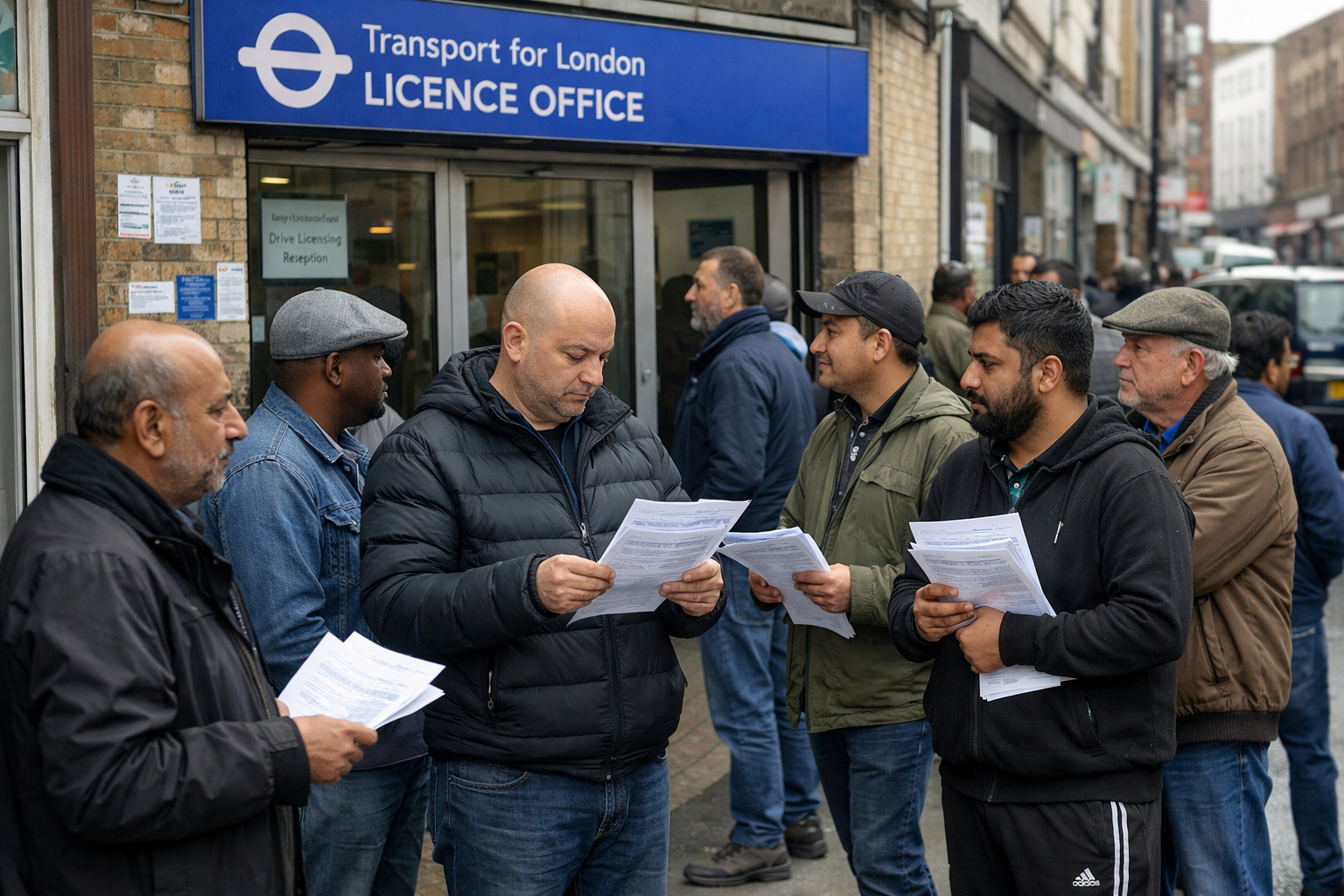

London’s private‑hire and taxi sectors are under pressure from two fronts right now: mounting delays in licence processing and strong enforcement of safety standards. Both are having real effects on drivers’ ability to work and on operators’ capacity to meet passenger demand. Licence Delays Affecting Income and Service Availability Many drivers in London report waiting months for new or renewed private‑hire licences. These delays have been raised formally in Parliament, but the Transport Minister has said central government won’t intervene directly in Transport for London’s licensing process. As a result, TfL remains responsible for approving licences, leaving drivers in limbo when applications pile up. Long licence waits mean drivers can’t earn if they’re unable to work legally, and operators struggle to retain a full roster of drivers. For a city that relies heavily on private‑hire services for daily commuting, airport transfers and night‑time economy trips, this administrative backlog isn’t just a paperwork issue. It has practical consequences for supply, reliability and driver livelihoods. Stronger Safety Enforcement Signals Public Safety Prioritisation At the same time, regulators are showing they’re willing to enforce strict safety standards. Transport for London has revoked nearly 500 private‑hire driver licences over the past year, including for serious offences such as drink‑driving, drug disqualifications and sexual misconduct. TfL’s “fit and proper” framework allows it to remove a licence without waiting for a court conviction when there is a clear safety concern. This enforcement sends a clear message: safety matters. It also highlights the differences in regulatory rigour between London and other regions, where licensing standards and enforcement vary. What This Means for Drivers Drivers need to be aware of two separate but intertwined realities. First, licence processing times are taking longer, which can stall work and earnings. Planning ahead for renewals and keeping application documents up to date can help reduce some delays. Second, maintaining high safety and conduct standards isn’t negotiable. Instances of serious misconduct are being acted upon swiftly, which protects passengers but also means drivers must ensure they meet TfL’s fitness criteria at all times. Advice for Operators and Brokers Operators should watch licence pipeline times closely and align driver recruitment, onboarding and rostering with expected processing timelines. Brokers and financing partners should factor in potential service gaps when modelling revenue and fleet utilisation. A driver‑short period can reduce bookings and affect vehicle revenue forecasts. Staying Ahead Keeping communication open with drivers and anticipating regulatory requirements will help mitigate some of the pressure. London’s private‑hire market is a complex ecosystem. Licence delays and safety enforcement are challenging right now, but they also reinforce a system that prioritises passenger safety and trust. That credibility is essential if the sector wants to adapt to future innovations like app‑based dispatching or autonomous vehicles.

Why charging matters now The UK’s electrification of transport is undeniable, but the recent Financial Times analysis stresses a tough reality: the country needs a dramatically faster rollout of electric vehicle (EV) charge points to meet demand by 2030. The current stock of about 88 000 public chargers is significant, yet official projections suggest a need of between 250 000 and 550 000 by decade’s end. To get close to even the lower threshold requires installations roughly double what the sector delivered in 2025. For planners, fleet managers and asset finance professionals, the charger rollout isn’t some abstract target — it’s a core infrastructure variable that silently shapes operating windows, cost assumptions and utilisation models. Without robust, widespread charging infrastructure, the total cost of ownership for EV fleets remains uncertain and risk appetites stay constrained. What the numbers mean for fleets Electric vehicles are fundamentally different to combustion engine vehicles in how they interact with infrastructure. An ICE vehicle can refuel at thousands of petrol stations almost anywhere. EV's require dedicated charging, and differences in charger speed, availability and location directly affect route planning. If you’re modelling a delivery or van fleet’s operating cost, you need clear assumptions on charger access and reliability. Having to detour for charging or facing queues at key nodes adds hours of unproductive time, which shows up in operating costs and asset utilisation. That, in turn, feeds directly into residual value forecasts and leasing terms. The FT piece points out that rural areas like Wales and Scotland are particularly underserved. That’s exactly where many operators — municipal contractors, rural delivery firms and regional logistics hubs — are already feeling the pinch in planning there transitions. Government pledges and industry concerns The Department for Transport has allocated £981 million to support the national charging network, with £381 million targeted to underserved areas and £600 million to accelerate broader deployment. Those numbers matter, but only if matched by predictable policy and implementation timelines. Industry groups have urged more enforceable targets and reduced VAT on public charging. Currently, public charging carries standard VAT, inflating user costs relative to home charging. These economic signals matter; they affect charging behaviour, investment decisions and where fleets choose to locate assets. If the government expects vans, cars and even heavier electric trucks to hit the road at scale, it has to reduce the economic penalty of public charging and make installations predictable for investors. Practical steps for finance teams Asset finance professionals need to treat infrastructure as a variable, not a given. Here’s how that looks in practice: Stress test residuals: Build scenarios with constrained charger availability and slow rollout timelines. That improves visibility on downside risk if adoption slows or operating costs remain high. Adjust utilisation curves: Include dwell time at chargers as a factor in productivity models. For high‑use fleets, extended charging time shifts revenue expectations. Engage on policy signals: Contact local and national policymakers to stay abreast of rollout plans. Greater clarity feeds directly into more accurate pricing models. Consider geography: A charger distribution skewed toward urban centres changes the economics of rural and regional operations. Debt and lease terms should reflect these locational risks. Broader implications beyond vans The charging challenge isn’t confined to vans or passenger cars. Medium and heavy duty fleets electrifying over the next decade will be subject to the same infrastructure constraints, only magnified by higher power requirements and longer dwell times. Even if early adopters demonstrate performance benefits, a slow public charging network will divert fleet investment toward private depot charging — a different asset class with its own financing implications. That influences working capital needs, lease structuring and the type of collateral lenders are willing to accept. Bottom line The UK’s charging rollout is more than a tech build. It’s a foundational piece of transport infrastructure that directly affects fleet economics, financing models and strategic planning. To hit net zero and support broader EV adoption, the country must not only install more chargers, but deliver clearer, more predictable signals on timing and scale. For anyone involved in asset finance or operations, this issue deserves attention today, not in some distant 2030 planning session. Source: Financial Times https://www.ft.com/content/611599ea-9e61-4366-881b-d66126f9f185

The UK taxi and private hire sector is facing fresh tension as drivers prepare for a coordinated, UK‑wide strike against Uber. The App Drivers’ and Couriers’ Union has urged private hire drivers to log out of the Uber platform for 24 hours in early February in protest at new pricing and commission terms introduced in January. Drivers are concerned that commissions on some rides can reach nearly half of gross fares, squeezing earnings and widening the gap between driver costs and take‑home pay. This strike reflects broader structural shifts in the UK taxi industry. Competition from global ride‑hailing platforms has reshaped work patterns for drivers, while local councils and regulators push back against practices they say undermine fair competition. Uber’s terms form part of broader platform changes that also include adjustments to pricing transparency, driver engagement and service availability. With tight margins already a challenge for private hire drivers, the new terms have intensified calls for clearer protections and more equitable share of fare revenue. One of the most visible signs of regulatory pressure on platforms is Uber’s recent withdrawal from Southend, where the company surrendered its private hire operator licence after facing local licensing conditions deemed too demanding to meet. The move highlights the growing role that city and council rules play in defining where and how ride‑hailing platforms can operate. Local licensing conditions vary across England and can influence driver earnings, safety standards and consumer fares. Drivers’ unions argue that a fair taxi ecosystem depends on transparent, consistent licensing and operations, with drivers earning a sustainable income. The union strike is an attempt to focus attention on the imbalance between platform gains and driver returns. While platforms argue that flexible engagement and digital dispatching benefits drivers and passengers, the tension underscores a need for more balanced dialogue. In response, some industry bodies are urging constructive negotiation. They point out that driver retention and satisfaction are crucial for reliable service levels and overall passenger confidence in ride‑hailing. Operators and local fleets may be better positioned to provide stable conditions by working directly with councils on licensing terms, fare setting and safety standards. The strike also comes at a time when automated vehicle pilots are gaining momentum in UK cities. Autonomous taxis, if introduced at scale, could eventually reduce dependence on human drivers altogether, changing the economics of ride‑hailing and private hire. For now, though, income pressures remain a central driver concern. Overall, the protest highlights how labour terms, licensing conditions and global platform strategies intersect in today’s UK taxi market. Drivers, operators and policymakers will need to work together to ensure that the industry remains viable, equitable and responsive to both driver welfare and passenger demand.